Modern economies are deeply dependent on a variety of raw materials, of which copper is one of the key ones. This metal has played an irreplaceable role in many areas of life for centuries, from the electrical industry to construction and information technology. Despite this, the price of copper has hardly changed over the course of 2023. We take a closer look at what shapes copper prices, what factors have the greatest impact on the copper market and what can we expect from the price of this metal in 2024?

Table of contents:

- What does the global copper market look like?

- What drives the price of copper?

- How will the copper price evolve in 2024?

What does the global copper market look like?

Copper is an important metal, widely used in a variety of industries due to its unique chemical properties and conductivity. Unlike many raw materials, it is not ready-to-use, requiring a number of processing steps before it is finally used. In most financial markets, we speak of end-use (End-Use) copper. For this reason, an increase in mining (supply) does not necessarily translate into a sudden and drastic fall in the price of copper on the financial markets.

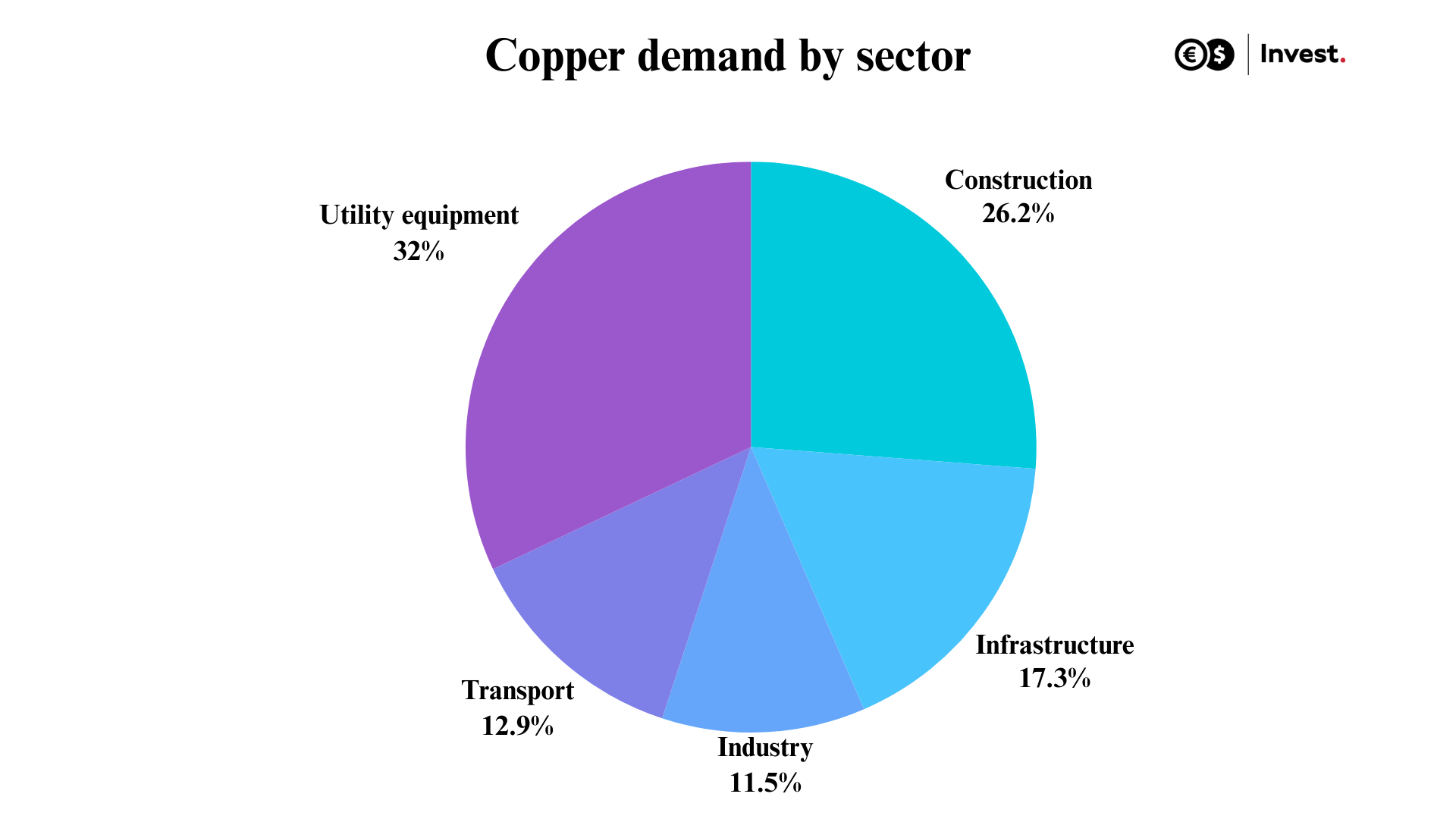

Data from the International Copper Association (ICA) for 2022 shows that the sector with the highest demand for copper is the consumer equipment industry, which includes industrial and commercial electronics, computers and telephones, accounting for an impressive 32% of total demand. In second place is the construction sector, with a focus on the areas of power, grounding, lighting and conduit installation, which accounts for 26.3% of total demand. The third place on the podium is occupied by the infrastructure sector, focusing mainly on utility transmission and distribution networks, with a share of 17.3%.

Source: Conotoxia, International Copper Association (ICA) Data

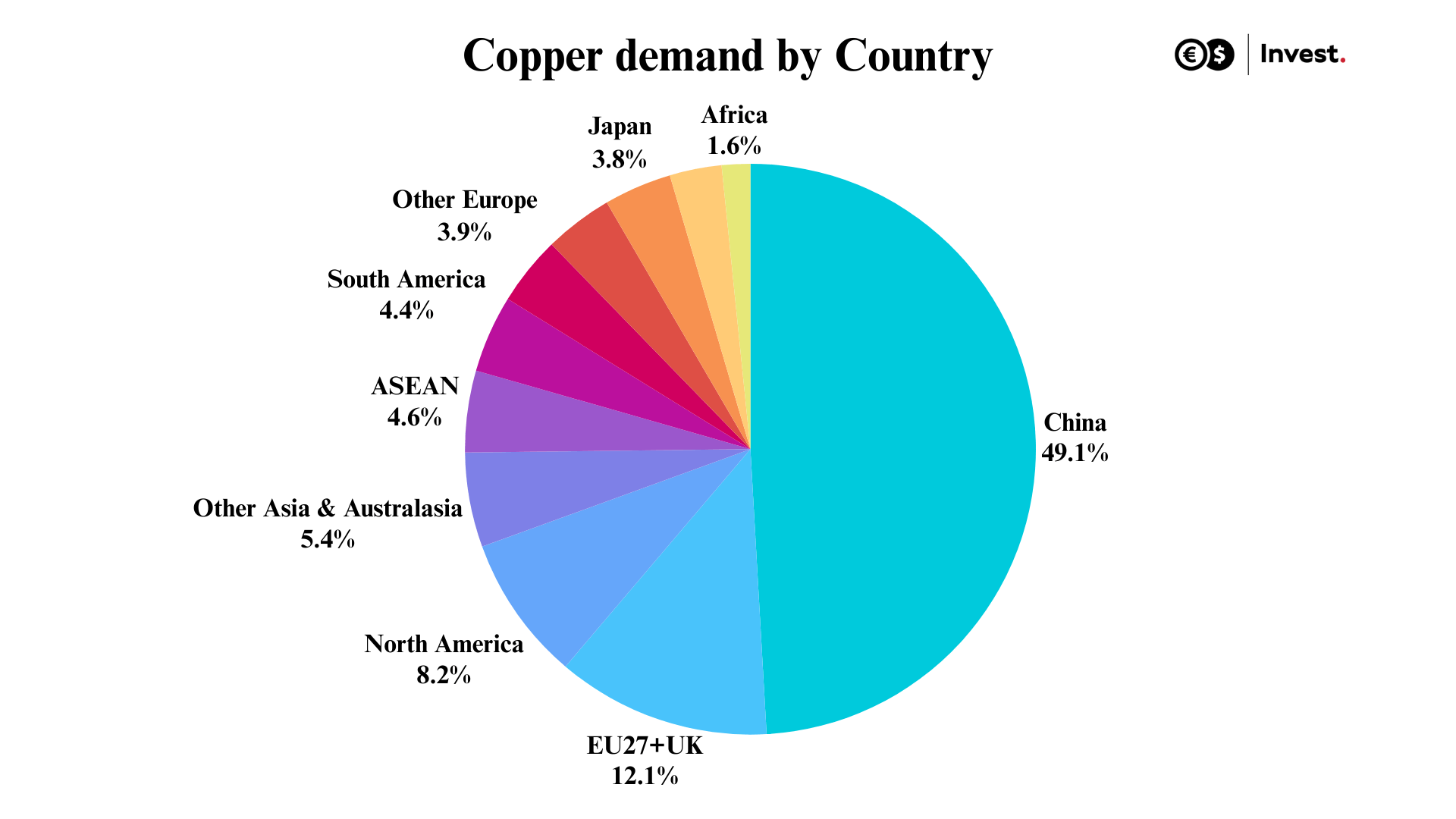

The largest demand for copper comes from China, which absorbs as much as 49.1% of global demand for the commodity. In second place is the European Union together with the United Kingdom, responsible for 12.1%, and North America closes the podium, mainly through demand from the United States (8.2%).

Source: Conotoxia, International Copper Association (ICA) Data

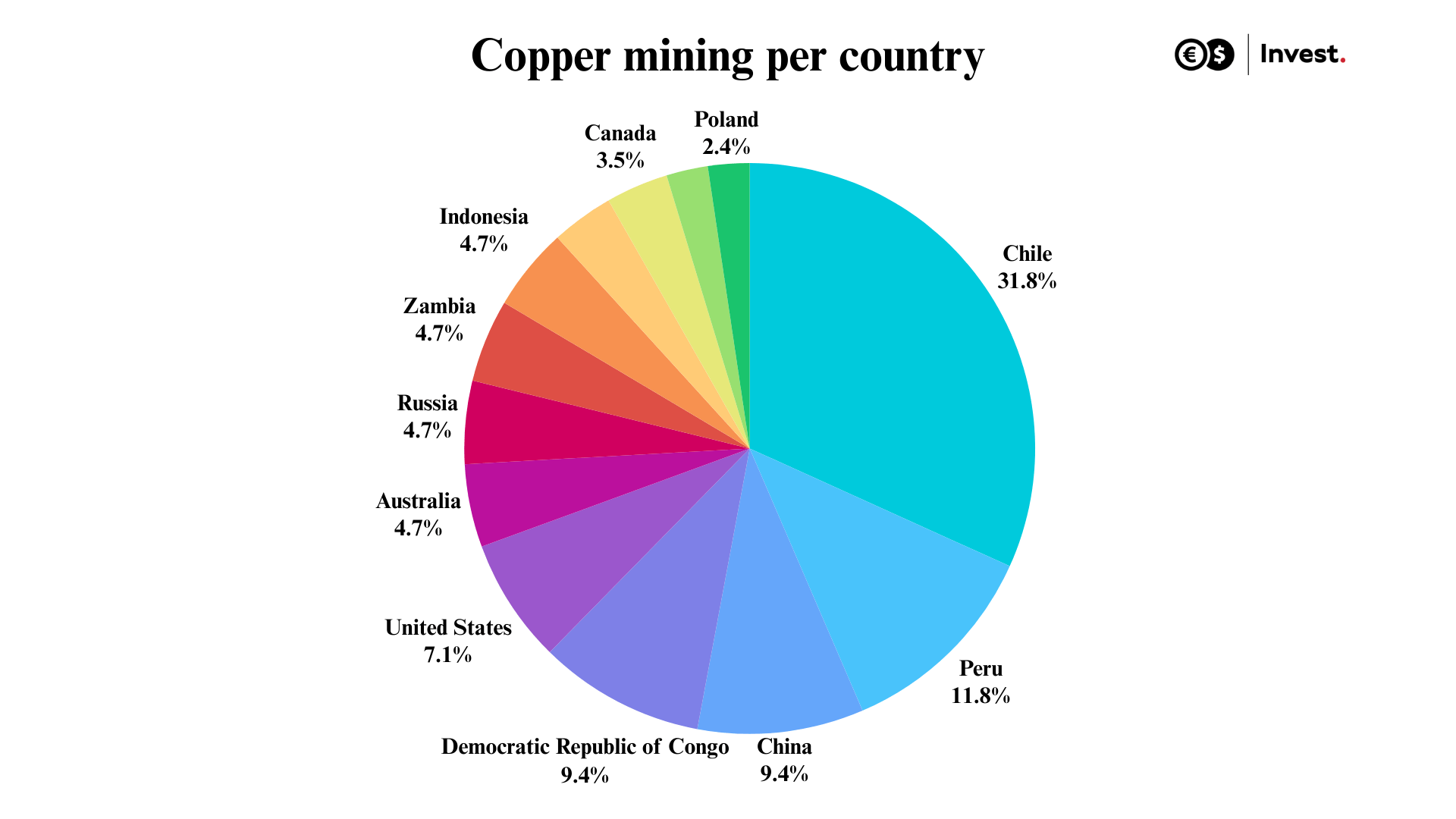

According to Statista, the largest producers of the resource are Chile, where mines account for 31.8% of global output. Peru ranks second with a share of 11.8%. Third place ex aequo is occupied by China and the Democratic Republic of Congo, both with 9.4% of global output.

Source: Conotoxia, Statista data

What drives the price of copper?

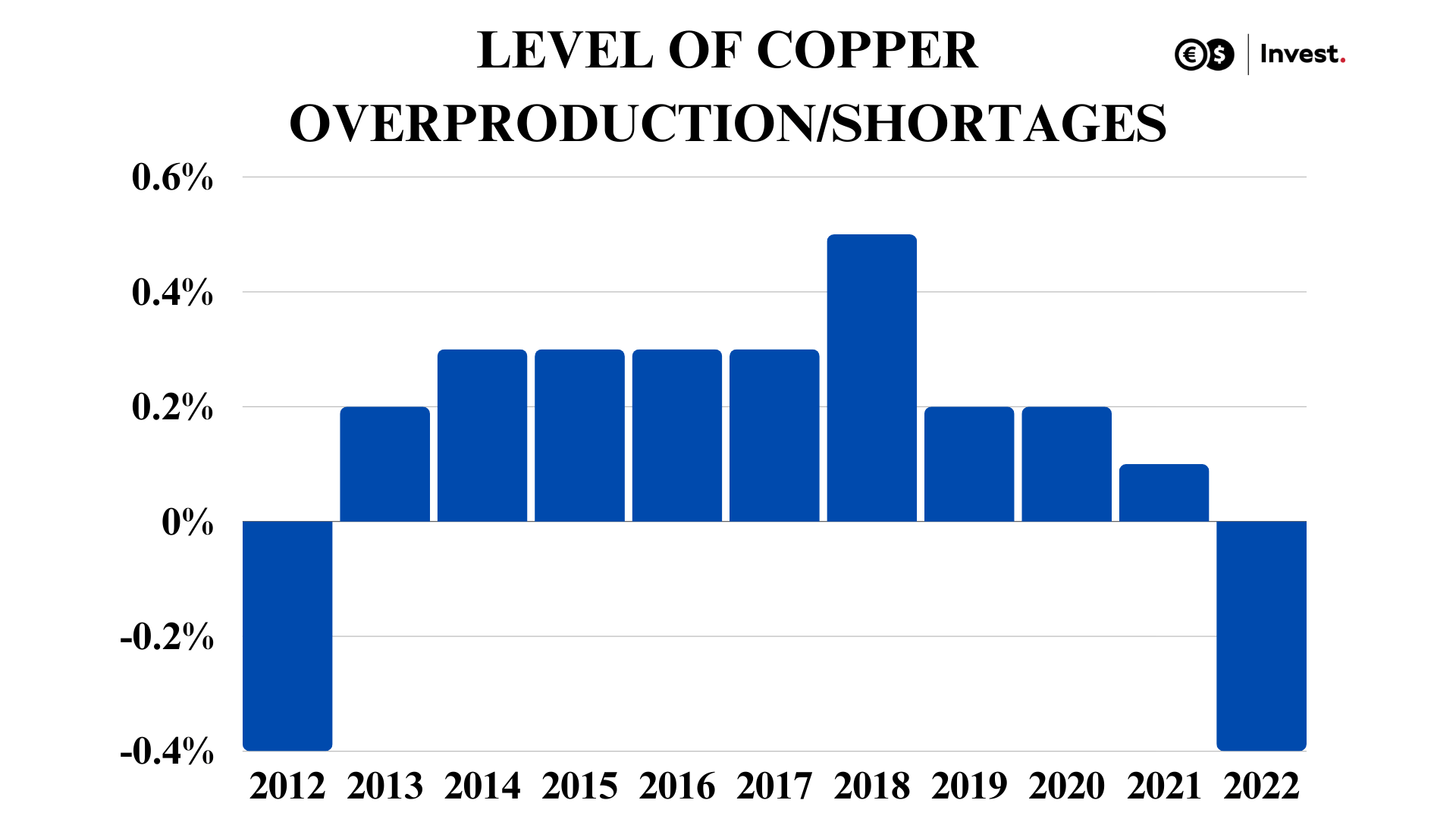

The price of copper, as with any good, is driven by the relationship between demand and supply. The global copper market has been characterised by many years of stability. We know from ICA data that total supply (mining and recycled recovery) in this market has not exceeded more than 0.5% of demand volumes since 2012. By comparison, in the oil market, the OPEC cartel's forecast for 2024 assumes a shortfall of as much as 2.2% of demand volumes. This would explain the much lower level of volatility in the copper price relative to energy commodities.

Source: Conotoxia, International Copper Association (ICA) Data

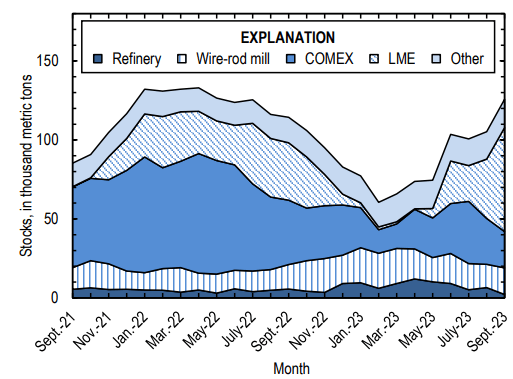

Final availability of refined copper in the US at the end of September 2023 increased by 10% compared to September 2022. Total stocks on the two largest exchanges (COMEX and London Metal Exchange Ltd.) increased by 34% in one month (September). This suggests a temporary oversupply of this commodity.

Source: Copper in September 2023, USGS

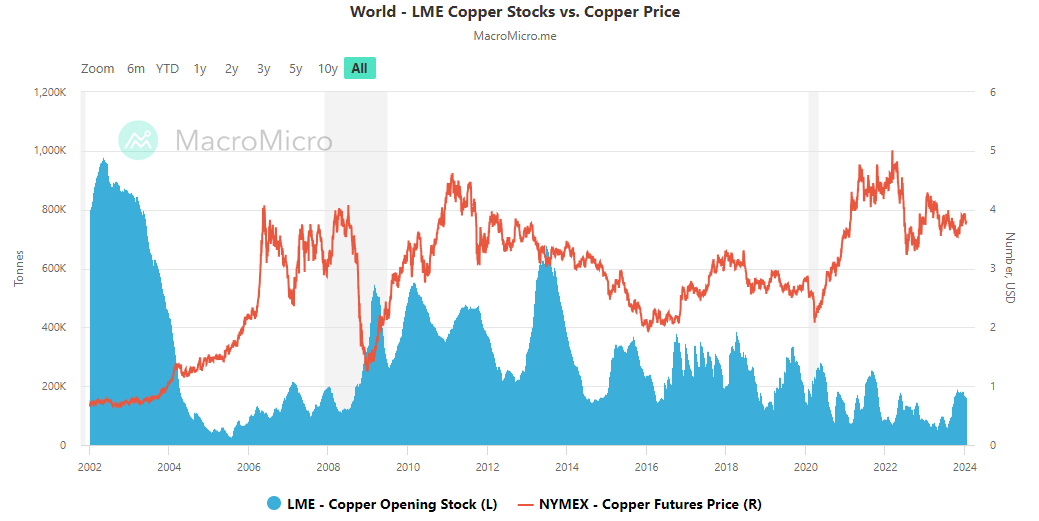

Despite this, for many years we have seen a gradual decline in copper stocks on the major commodity exchanges, which has had a positive impact on the copper price. It seems that a breach of the 200 000 tonnes level of copper stocks on the exchanges could be one of the first negative signals for the future copper price. For this to happen, the amount of stocks would have to increase by more than 60%, which does not seem possible in the coming months.

Source: MacroMicro

As the most important players in this market in terms of production are Chile, Peru and China (which together account for 53% of global extraction), and in terms of consumption practically only China with its industrial production (accounting for 49.1% of global demand), it is mainly the situation in these countries that would determine the copper price.

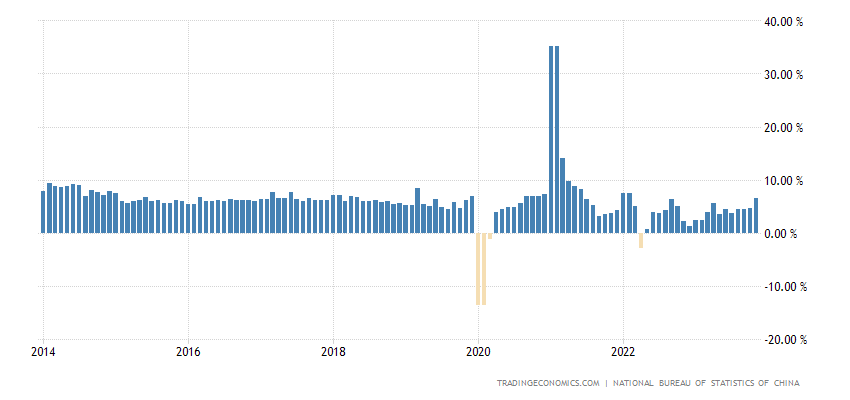

Global copper mining and processing remains relatively stable, growing by 2.5% per year since 2012. However, projections of data from Mining Technology indicate that global copper production would increase by 4.8% in 2024. This may explain the temporary increases in stocks on commodity exchanges. After all, most investors in this market are focusing their attention mainly on the situation in the Chinese industry, which is famous for its large infrastructure investments. This sector seems to be recovering again, growing by 6.6% y/y in November 2023 after a temporary stagnation.

Source: Tradingeconomics, China industrial production

How will the copper price evolve in 2024?

For copper to become materially more expensive, there would have to be either a surge in global production, which would return to the long-term growth rate of this market after the pandemic-induced slowdown, or a collapse in production. Both of these scenarios seem unlikely at the moment, as both industrial production in China, which generates as much as 49.1% of global copper demand, has returned to its long-term growth rate and mining is maintaining its growth rate. Therefore, at the moment, there are no significant factors that would suggest a drastic change in the price in 2024. Nevertheless, it could be a one-sided game at the moment, due to potential supply or mining disruptions. As such, we are likely to see gradual increases in the price of this commodity on commodity exchanges, as China's annual industrial production growth rate of 6% on average outpaces the 2.5% increase in extraction. Moreover, a side effect of this could be a further increase in China's share of global copper demand.

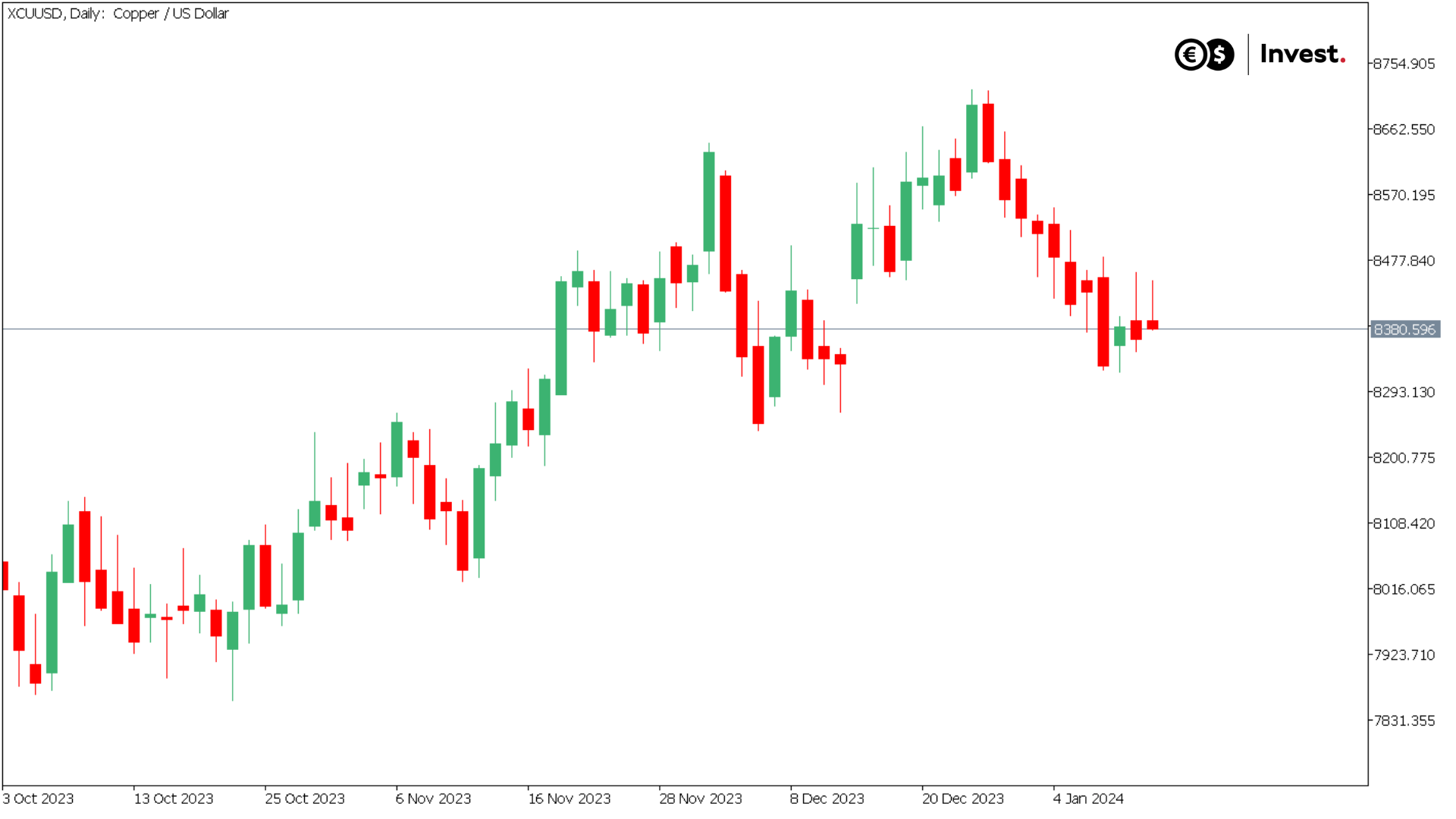

Source: Conotoxia MT5, XCUUSD, Daily

Grzegorz Dróżdż, CAI MPW, Market Analyst of Conotoxia Ltd. (Conotoxia investment service)

Materials, analysis and opinions contained, referenced or provided herein are intended solely for informational and educational purposes. Personal opinion of the author does not represent and should not be constructed as a statement or an investment advice made by Conotoxia Ltd. All indiscriminate reliance on illustrative or informational materials may lead to losses. Past performance is not a reliable indicator of future results.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71.98% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Trade this news from Conotoxia Ltd. platforms

Go to your account