It turns out that Japan's economy, the third most powerful in the world, contracted much more than analysts had predicted - by 0.7% quarter-on-quarter. This resulted in a flurry of sell-offs on the USD/JPY exchange rate, which saw a 2.4% decline. The second major piece of news last week was the continuation of the decline in US CPI inflation to 3.2%, down from the previous 3.8%. Looking at the global data, it appears that the economic slowdown in many countries is contributing to a lower rate of price growth. The coming week will be marked by interest rate decisions by six major central banks, including: US, Eurozone, UK or Switzerland.

Table of contents:

- US consumer price index (CPI) annualised (November)

- US interest rate decision

- Switzerland interest rate decision

- UK interest rate decision

- Eurozone interest rate decision

- Stocks to watch

Tuesday, 12.12, 13:30 GMT, US consumer price index (CPI) annualised (November)

The CPI monitors changes in the prices of consumer goods and services. The CPI is an important indicator because it helps us to understand trends in consumers' purchases and the impact of inflation on their purchasing power. It is calculated on the basis of a basket representing typical consumer spending, covering various categories such as food, housing, transport, etc. Regular measurements of the CPI allow us to track how the prices of these products and services change over time. A positive CPI indicates an overall increase in the prices of goods and services.

On the other hand, a negative CPI means that prices are lower than the year before. It is an important tool for economists and policymakers to help them understand the impact of inflation on the economy and take appropriate action. For consumers, it is information about how their money is losing value in the context of rising or falling prices, allowing them to adjust spending, plan savings and make financial decisions.

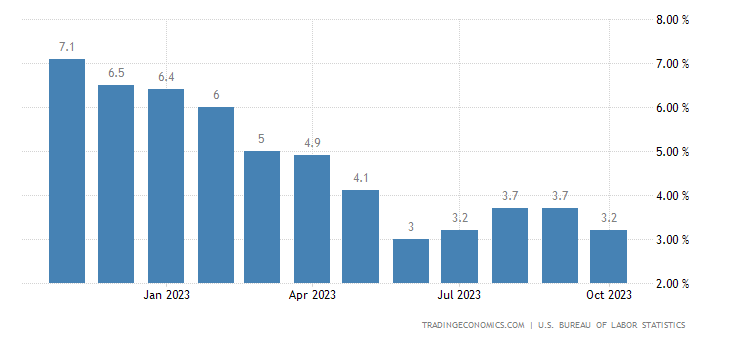

In October 2023, the US annual inflation rate fell to 3.2% from the 3.7% recorded in August and September. Market forecasts called for a reading of 3.3%. The decline in inflation was mainly due to a 4.5% reduction in energy costs, including gasoline down 5.3%, gas services down 15.8% and heating oil down 21.4%. The CPI remained almost unchanged compared to September. However, the underlying CPI (which excludes fuel and food prices) was up 4% on an annual basis and up 0.2% on a monthly basis, which was below forecasts of 4.1% and 0.3% respectively. The current consensus of TradingEconomics analysts is for a symbolic decline in CPI inflation to 3.1% and for its underlying counterpart to remain at 4%.

Source: Tradingeconomics.com

A higher-than-expected reading could have a bullish impact on the USD, while a lower-than-expected reading could be bearish for the USD.

Impact: USD

Wednesday, 13.12, 18:00 GMT, US interest rate decision

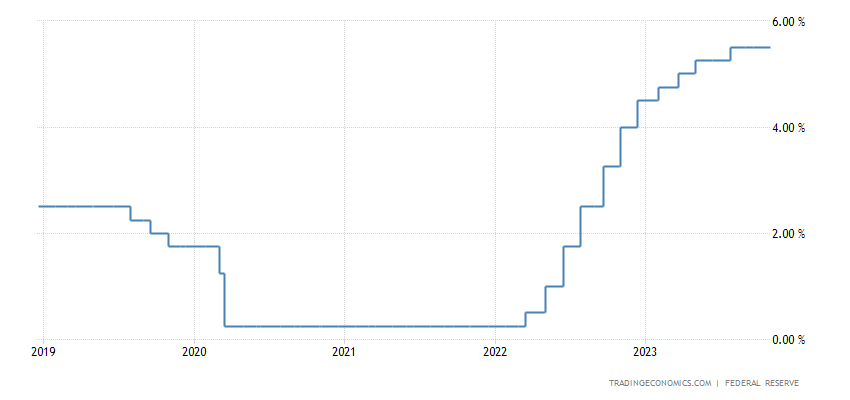

"It would be premature to say with confidence that we have reached a sufficiently restrictive stance or to speculate on when policy might ease," - Fed chairman Jerome Powell said at a recent speech. According to the FedWatch tool, which measures the market's valued probability of interest rate changes, with a 58.4% probability the market is pricing the first cut as early as March 2024, and with as much as 86.2% in May. The current analyst forecast is that interest rates will remain unchanged at the next FOMC meeting.

Source: Tradingeconomics.com

Higher-than-expected interest rates could be positive for the USD and negative for the equity market, while lower-than-expected interest rates could be negative for the USD and positive for the equity market.

Impact: USD, S&P 500

Thursday, 14.12, 8:30 GMT, interest rate decision in Switzerland

At its latest meeting in September, the Swiss National Bank held its benchmark interest rate steady at 1.75%. The Bank said that the significant tightening of monetary policy in recent quarters had effectively counteracted ongoing inflationary pressures. The decision interrupted the rate hike campaign that began last June, surprising market expectations of another 25bp hike. Nonetheless, policymakers added that further monetary tightening is not ruled out to ensure price stability in the medium term, and they will keep a close eye on inflation developments in the coming months.

Inflation forecasts have been maintained at 2.2% for both 2023 and 2024, while GDP growth in the Swiss economy this year is forecast at around 1%, a slight change from previous forecasts. Switzerland's annual inflation rate remained at 1.6% in August, remaining the lowest since January 2022, while the economy stalled in Q2 this year. Currently, analysts' consensus is for no change in interest rates, which would imply a continuation of the 'wait and see' strategy.

Source: Tradingeconomics.com

Higher-than-expected interest rates could be positive for the CHF, while lower-than-expected interest rates could be negative for the CHF.

Impact: CHF

Thursday, 14.12, 12:00 GMT, UK interest rate decision

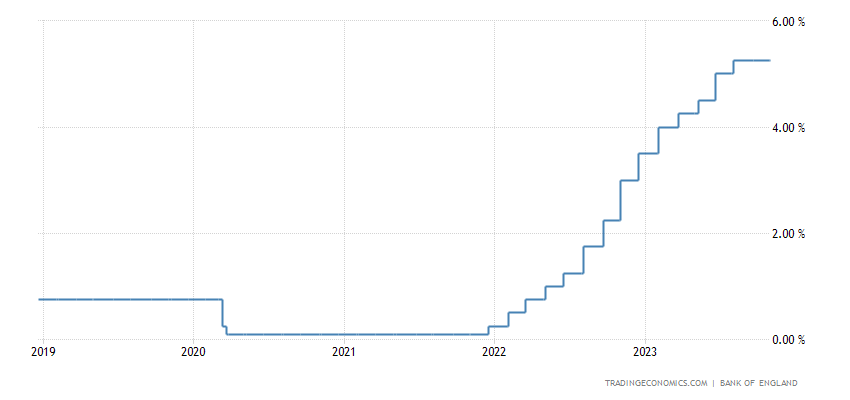

The Bank of England kept its benchmark interest rate unchanged at 5.25% for the second consecutive month at its November meeting. Policymakers took this decision given the recent signs of economic slowdown in the UK, evident in the decline in GDP growth to 0.6% year-on-year. At the same time, they are facing the ongoing challenge of CPI inflation, which, although declining, is still at 4.6%.

The central bank additionally stressed that monetary policy is likely to remain restrictive for an extended period to steer inflation back towards the 2% target. Policymakers stressed their readiness to implement further tightening measures if needed. Currently, the consensus among analysts is for the Bank of England to maintain the current level of interest rates.

Source: Tradingeconomics.com

Higher-than-expected interest rates could be positive for the GBP and negative for the equity market, while lower-than-expected interest rates could be negative for the GBP and positive for the equity market.

Impact: GBP, UK100

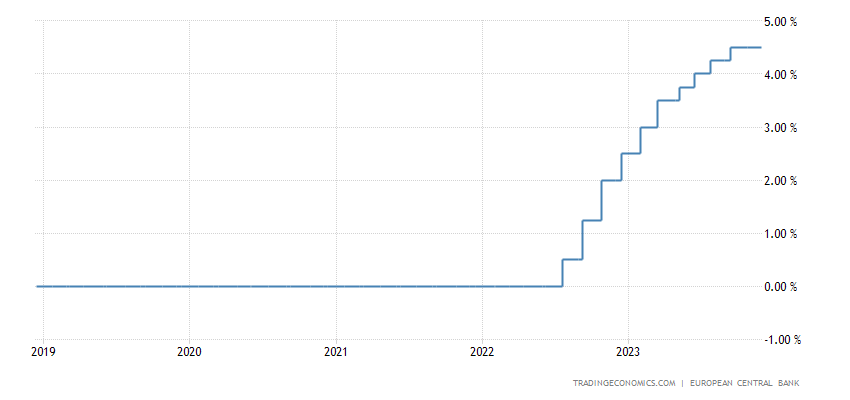

Thursday, 14.12, 13:15 GMT, Eurozone interest rate decision

The European Central Bank (ECB) held interest rates steady at its October meeting, a change from a 15-month series of rate hikes. This decision reflects a more cautious stance by policymakers, responding to the gradual easing of price pressures and concerns about an impending recession. Recent GDP readings point to a 0% year-on-year growth rate. Prior to the October meeting, there had been ten interest rate rises since July 2022. As a result, the main refinancing operations rate rose to its highest level in 22 years at 4.5% and the deposit rate reached a record high of 4%.

The central bank has stated that it is determined to ensure that CPI inflation returns to its 2% target in the medium term, currently at 2.4%. The ECB now appears to be moving closer to this target. This new stance is a reaction to changing economic conditions and aims to offset inflationary pressures while avoiding the possible effects of an impending recession. Nonetheless, the current consensus of analysts does not yet foresee a change in interest rates in response to the weakening economic situation in the euro area.

Source: Tradingeconomics.com

Higher-than-expected interest rates could be positive for the EUR and negative for the equity market, while lower-than-expected interest rates could be negative for the EUR and positive for the equity market.

Impact: EUR, DAX

Stocks to watch

Oracle (ORCL) announces financial results for the quarter ending December 2023. Forecast EPS: 1.32. Positive earnings surprise in 8 of last 10 reports. Deadline: Monday, 11 December.

Adobe (ADBE) announces financial results for the quarter ending December 2023. Forecast EPS: 4.13. Positive earnings surprise in 10 of last 10 reports. Deadline: Wednesday, 13 December.

Costco (COST) announces financial results for the quarter ending November 2023. Forecast EPS: 3.4. Positive earnings surprise in 8 of last 10 reports. Deadline: Thursday, 14 December.

Grzegorz Dróżdż, CAI MPW, Market Analyst of Conotoxia Ltd. (Conotoxia investment service)

Materials, analysis and opinions contained, referenced or provided herein are intended solely for informational and educational purposes. Personal opinion of the author does not represent and should not be constructed as a statement or an investment advice made by Conotoxia Ltd. All indiscriminate reliance on illustrative or informational materials may lead to losses. Past performance is not a reliable indicator of future results.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.95% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.