After the Thanksgiving holiday in the US, next week will see the release of some important macroeconomic data, such as US GDP growth for the third quarter, which may confirm the estimated 4.9% increase. Furthermore, the New Home Sales, together with the US CB Consumer Confidence Index report, may provide us with the newest insight into consumer confidence levels in the US. Meanwhile, the preliminary data for the Eurozone's inflation level in November will be coming out later next week.

Table of contents:

- US New Home Sales (October)

- US CB Consumer Confidence (November)

- US Gross Domestic Product (GDP) QoQ (Q3)

- Eurozone Consumer Price Index (CPI) YoY (November preliminary)

- Stocks to watch

Monday 27.10. 15:00 GMT, US New Home Sales (October)

New Home Sales is an economic indicator published by the US Census Bureau that measures the number of new home sales, taking into account any deposits paid or contracts signed on single-family homes built in the current or previous year. A high number would indicate that the housing activity may be high, leading to strong economic growth. Although a lagging indicator, new home sales are closely watched by investors as they represent consumer demand driven by factors like interest rates, unemployment, and household income. New Home Sales are reported in absolute terms and as a percentage change from the previous month. In addition, new home sales are usually released before Existing Home Sales, as the two data are closely correlated.

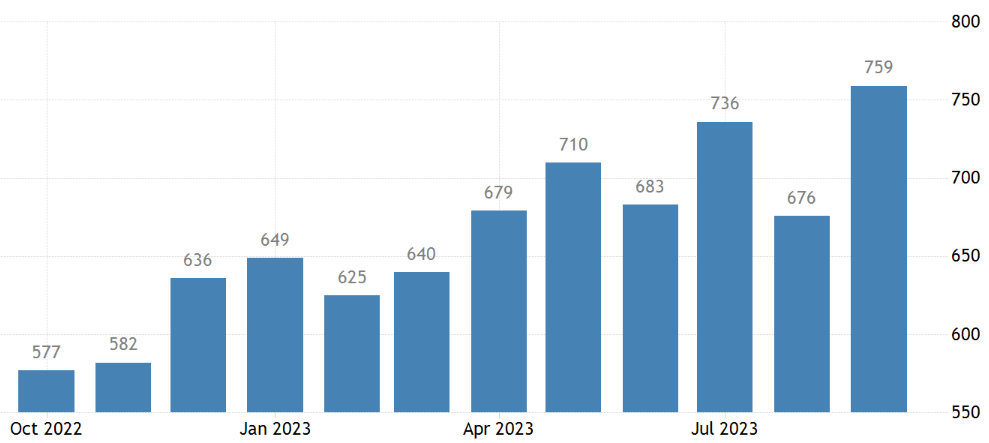

Sales of newly built single-family homes in the United States showed a notable increase, rising 12.3% to a seasonally adjusted annualised rate of 759 thousand in September 2023. This was a significant rebound from the previous month's revised figure of 676 thousand and exceeded the market consensus of 680 thousand. This robust performance represents the highest level of new home sales since February 2022. The consensus forecast for the upcoming report is for 730 thousand, which would represent a slight decline from the previous month's surge.

The heightened demand for new housing and homebuilding might be attributed to a shortage of previously owned houses in the market. Sales exhibited growth across all regions, with the South leading at a 14.6% increase to 456 thousand, followed by the West with a 7.5% rise to 187 thousand, the Midwest with a 4.7% uptick to 67 thousand, and the Northeast recording a substantial 22.5% increase to 49 thousand.

The median price of newly sold houses stood at 418,800 USD, while the average sales price was 503,900 USD. In comparison to the figures from a year ago, this reflects a change from 477,700 USD to 418,800 USD for the median price and from 530,100 USD to 503,900 USD for the average price. As of the end of September, the inventory revealed that 435 thousand houses were still available for sale.

Source: Tradingeconomics.com

A higher-than-expected reading may have a bullish effect on the USD, while a lower-than-expected reading could be bearish for the USD.

Impact: USD

Tuesday, 28.11. 15:00 GMT, US CB Consumer Confidence (November)

The Conference Board's Consumer Confidence Index (CCI) measures consumer confidence in the economy. It is an indicator that can predict future consumer spending, a key factor in overall economic activity. Higher values indicate greater consumer optimism. The CCI is measured based on the level of confidence in 1985, which was set at 100 points. An index above 100 points indicates a higher confidence level than in 1985. Conversely, a value below 100 points means a lower confidence level than in 1985.

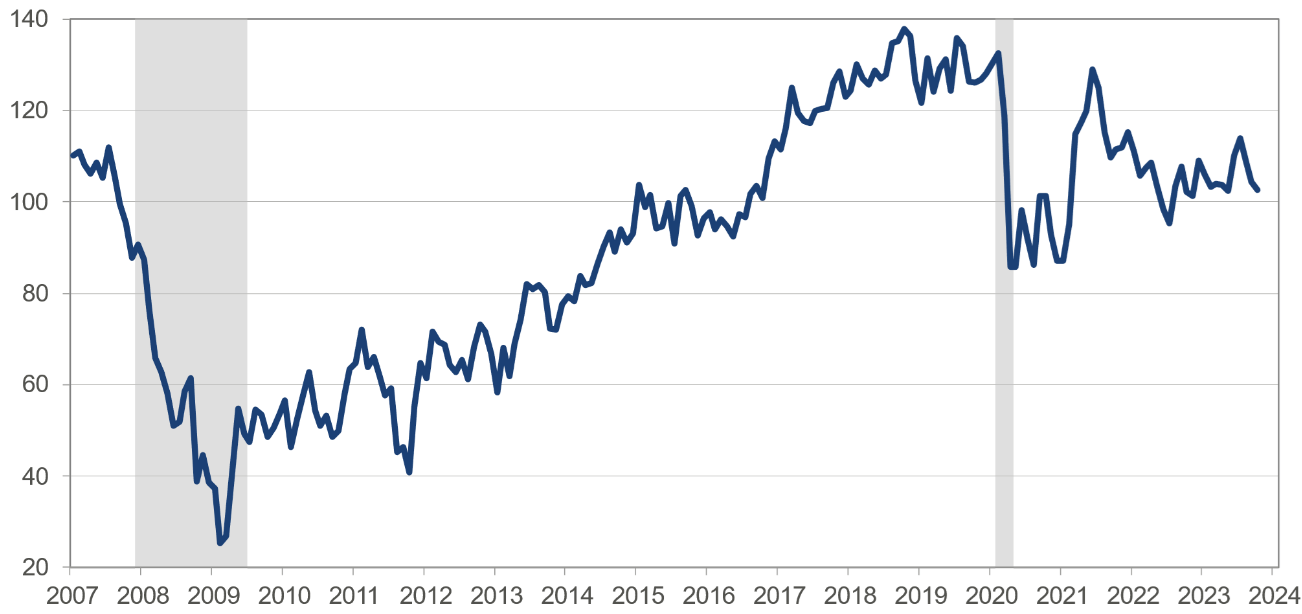

The Conference Board Consumer Confidence Index experienced a moderate decline in October, dropping to 102.6 (1985=100) from an upwardly revised 104.3 in September. The overall trend reveals a third consecutive month of decline in consumer confidence. Within this index, the Present Situation Index, which gauges consumers' evaluations of current business and labour market conditions, decreased to 143.1 (1985=100) from 146.2. Additionally, the Expectations Index, which reflects consumers' short-term outlook for income, business, and labour market conditions, saw a slight dip to 75.6 (1985=100) in October, following a decline to 76.4 in September.

Notably, the Expectations Index remains below 80, a historical threshold indicating a potential recession within the following year. Consumer concerns about an impending recession persist at elevated levels, aligning with an anticipation of a short and shallow economic contraction in the first half of 2024.

Source: www.conference-board.org/

A higher-than-expected reading may have a bullish effect on the USD, while a lower-than-expected reading could be bearish for the USD.

Impact: USD

Wednesday 29.11. 13:30 GMT, US Gross Domestic Product (GDP) QoQ (Q3)

Gross domestic product (GDP) indicates the total value of goods and services produced in a country for a certain period. GDP is an important indicator of the health of an economy because it gives an overall picture of how well or poorly it is doing. If the GDP growth is higher than expected, the economy is in good shape and growing faster than expected. On the other hand, if the GDP growth is lower than expected, the economy performs weaker than anticipated. Furthermore, if the GDP growth is negative for two consecutive quarters, it may be considered a technical recession due to contracting economic output.

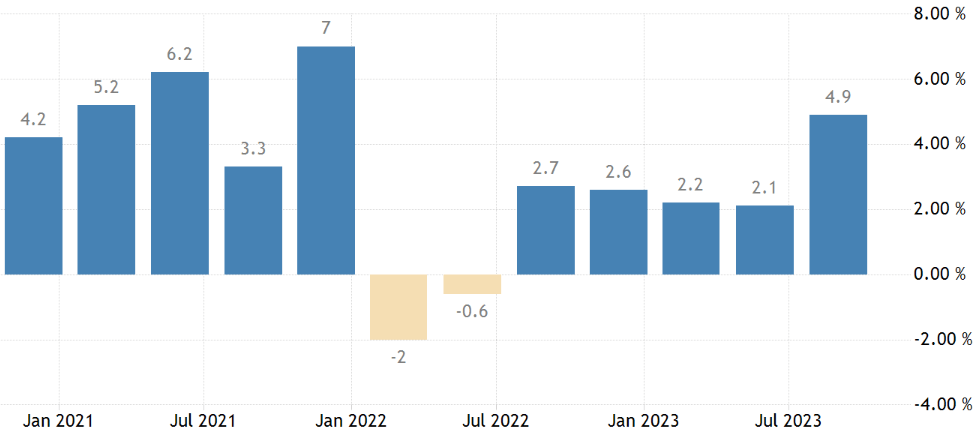

According to an initial estimate, the US economy demonstrated robust growth, expanding at an annualised rate of 4.9% in Q3 2023, marking the highest growth rate since the final quarter of 2021. This also exceeded market expectations of 4.3% and represented a significant increase from the 2.1% expansion observed in Q2.

Key drivers of this economic expansion included a notable 4% increase in consumer spending, the most substantial uptick since Q4 2021 (compared to 0.8% in Q2 2023). This surge in consumer spending was led by expenditures on housing and utilities, healthcare, financial services and insurance, food services and accommodation, as well as non-durable goods, particularly prescription drugs and recreational goods and vehicles.

The quarter also saw a notable rebound in exports, which rose by 6.2% after a 9.3% fall in the second quarter, while imports rose by 5.7%, compared with a fall of -7.6% previously. Private inventories made a significant contribution to growth, adding 1.32 percentage points - the first positive contribution in three quarters.

In addition, residential investment turned positive, growing at a rate of 3.9% (up from -2.2%) for the first time in almost two years, and government spending accelerated (up from 3.3% to 4.6%). In contrast, non-residential investment contracted for the first time in two years, falling by 0.1% (compared with growth of 7.4%), mainly due to a fall in equipment (3.8% compared with 7.7%) and a slowdown in structures (1.6% compared with 16.1%).

Source: Tradingeconomics.com

A higher-than-expected reading may have a bullish effect on the USD, while a lower-than-expected reading could be bearish for the USD.

Impact: USD

Thursday 30.11. 10:00 GMT, Eurozone Consumer Price Index (CPI) YoY (November preliminary)

The CPI index measures changes in the prices of consumer goods and services. It covers different types of products, such as food, fuel, transportation services, cosmetics, household goods, clothing, and many others. The purpose of the CPI index is to measure the increase or decrease in the cost of living for consumers. As the CPI index rises, consumers' purchasing costs increase, affecting their money's purchasing power. The CPI index is used to monitor inflation or the overall rise in prices in the economy. It allows us to assess whether prices are rising too fast or too slowly and to determine what economic policy measures should be taken to offset the adverse effects of inflation.

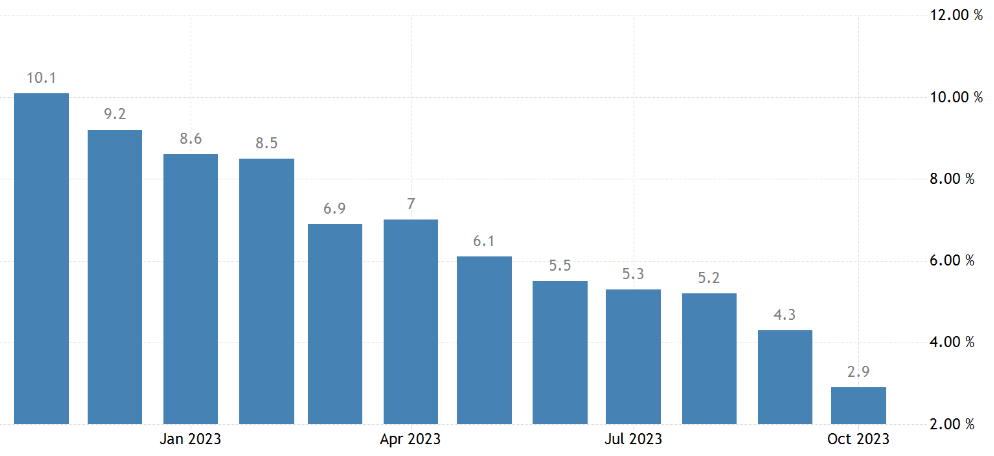

The inflation rate in the Eurozone for October 2023 was officially verified at 2.9% year-on-year. While this represents the lowest figure since July 2021, it still exceeds the European Central Bank's (ECB) target of 2%. The decline in energy prices and a deceleration in food inflation were the primary factors contributing to this outcome. Concurrently, the core inflation rate, which excludes the influence of volatile food and energy prices, also decreased to 4.2% in October, reaching its lowest level since July 2022.

Energy costs recorded a significant fall of 11.2%, a marked contrast to the -4.6% recorded in September. In addition, inflation rates eased in categories such as food, alcohol and tobacco (7.4% compared with 8.8%) and non-energy industrial goods (3.5% compared with 4.1%). Inflation in services remained relatively stable at 4.6%, compared with 4.7% in the previous month.

On a monthly basis, consumer prices exhibited a marginal increase of 0.1% in October, following a 0.3% rise in September.

Source: Tradingeconomics.com

If the reading is higher than expected, inflation is higher, possibly favouring a fall in the EUR. Meanwhile, it may be also a stimulus for the ECB to raise interest rates and reduce the money supply, causing an increase in the EUR. If the reading is lower than expected, it may give the ECB an argument to stop its policy of raising interest rates.

Impact: EUR, STOXX, DAX and other indices

Stocks to watch

Hewlett Packard (HPE) announcing its earnings results for the quarter ending on 10/2023. Forecast EPS: 0.4969. Positive earnings surprise in 8 out of the last 10 reports. Time: Tuesday, November 28, after the market closes.

Dollar Tree (DLTR) announcing its earnings results for the quarter ending on 10/2023. Forecast EPS: 7.55. Positive earnings surprise in 8 out of the last 10 reports. Time: Wednesday, November 29, before the market opens.

Marvell (MRVL) announcing its earnings results for the quarter ending on 10/2023. Forecast EPS: 0.4006. Positive earnings surprise in 8 out of the last 10 reports. Time: Friday, December 1.

Santa Zvaigzne-Sproge, CFA, Head of Investment Advice Department at Conotoxia Ltd. (Conotoxia investment service)

Materials, analysis, and opinions contained, referenced, or provided herein are intended solely for informational and educational purposes. The personal opinion of the author does not represent and should not be constructed as a statement, or investment advice made by Conotoxia Ltd. All indiscriminate reliance on illustrative or informational materials may lead to losses. Past performance is not a reliable indicator of future results.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.95% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.