The latest inflation readings from the Eurozone and the United States appear to be encouraging. It looks like we are getting closer and closer to a possible change in monetary policy by the Fed, as can be seen on the CME Group's interest rate probability barometer. Currently, the market is predicting with a 76 per cent probability that there might not be a hike at the next FOMC meeting, and the first cut could come as early as the end of this year. To better prepare for this situation, it is worth considering how history has shaped the prices of individual asset classes before and after the change in interest rate trajectory.

The "fool in the shower" theory

But let's start by answering the question: are central banks as effective in their decision-making as we think? It turns out that a rather good analogy was cited by Nobel laureate Milton Friedman, who compared overly radical central bank action to the behaviour of a fool while taking a shower. When central banks or governments react too strongly to fluctuations in the economic cycle and loosen/tighten monetary and fiscal policy too quickly, without waiting to assess the effects of their initial actions, they behave like someone who realises the water is too cold and turns on the hot water. However, the hot water takes a while to arrive, so they simply turn the hot water up to maximum, which eventually leads to scalding. Looking at historical interest rate levels, this is easy to see. For this reason, let's only consider the peaks for examining periods of initial reductions.

Since the 1970s, seven significant peaks of this type have been observed: in 1974, 1980, 1984, 1989, 2000, 2007 and 2019. However, it is noted that these peaks are not unambiguous, which can make it difficult to interpret when exactly the trend change occurred.

stopy_procentowe_06.06.png)

Source: FRED

Is it the stock that gains or loses at pivot?

One of the main assets affected by a change in the trajectory of interest rate policy is company shares. A change in the cost of debt has a direct impact on companies' operations. It is expected that a reduction in the cost should have a positive impact on companies. However, when analysing the behaviour of shares 2 months before and 2 months after the first reduction, it is difficult to make a clear statement about the impact of the reduction on the market. In some cases the cut resulted in an increase, while in other cases declines were observed on the S&P 500, Nasdaq Composite and Dax indices.

Source: Conotoxia Ltd own analysis based on Yahoo Finance data

Source: Conotoxia Ltd’s own analysis based on Yahoo Finance data

Source: Conotoxia Ltd own analysis based on Yahoo Finance data

Is the rate cut really weakening the dollar?

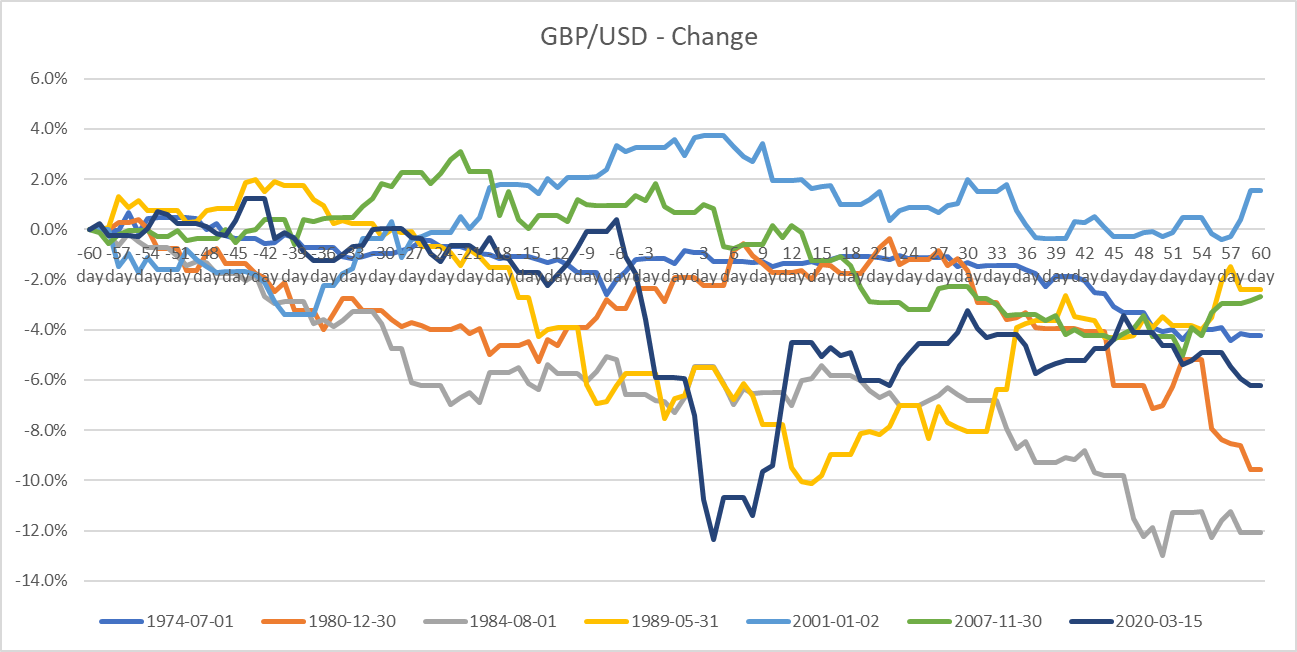

The foreign exchange market is another market that is directly affected by changes in interest rates. It is generally accepted that a currency whose interest rates are rising faster should strengthen relative to other currencies. Despite this, when analysing the behaviour of the US dollar against the European currency, it can be seen that since the 1970s, there has almost always been a strengthening of the dollar after an interest rate cut, resulting in a fall in the EUR/USD currency pair.

Source: Conotoxia Ltd own analysis based on Yahoo Finance data

This change is even more pronounced on the GBP/USD pair.

Source: Conotoxia Ltd own analysis based onYahoo Finance data

How do safe havens behave?

Safe havens is a term used in an investment context to refer to assets or financial instruments that are considered relatively safe and stable in times of economic uncertainty, such as changes in monetary policy. Investors seek safe havens as a way to protect their capital from potential losses. Examples of this type of asset include gold and bonds. The former, as can be seen in the chart below, sometimes rose and sometimes fell at the time of the Fed's pivot. It is therefore hard to determine any impact of this decision on the prices of this commodity.

Source: Conotoxia Ltd own analysis based on Yahoo Finance data

Interest rates have a direct impact on the valuations of government bonds, whose yields are expected to fall (and prices to rise) when interest rates are cut. And indeed such a trend has been observed for most of the reductions. However, the situations of the 1974 and 1980 crises seem to break out of this relationship. Here it is worth mentioning that the valuation of yields on, among other things, 10-year bonds is made up of 2 main factors, which are, the real yields on new bonds issued and the premium for the risk of possible default, which seemed to rise overnight in 74 and 80.

Source: Conotoxia Ltd own analysis based on Yahoo Finance data

Grzegorz Dróżdż, CAI, Market Analyst of Conotoxia Ltd. (Conotoxia investment service)

Materials, analysis and opinions contained, referenced or provided herein are intended solely for informational and educational purposes. Personal opinion of the author does not represent and should not be constructed as a statement or an investment advice made by Conotoxia Ltd. All indiscriminate reliance on illustrative or informational materials may lead to losses. Past performance is not a reliable indicator of future results.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.18% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Trade this news from Conotoxia Ltd. platforms

Go to your account