On 19 March, the Bank of Japan became the latest in the world to end its eight-year negative interest rate policy, raising short-term rates to 0-0.1%. This did not come as a surprise to market analysts, however, due to earlier announcements of the decision. The historic change marks the first rate hike in Japan since the 2008 crisis. Nonetheless, the USD/JPY exchange rate remains at relatively high levels (above 150), as does Japan's Nikkei 225 index. So let's consider how the change in monetary policy will affect the yen and Japanese equities in the coming months.

Table of contents:

- Problems of the Japanese economy

- The Bank of Japan holds its hand over the intervention button!

- The future of the Nikkei 225 and the USDJPY

Problems of the Japanese economy

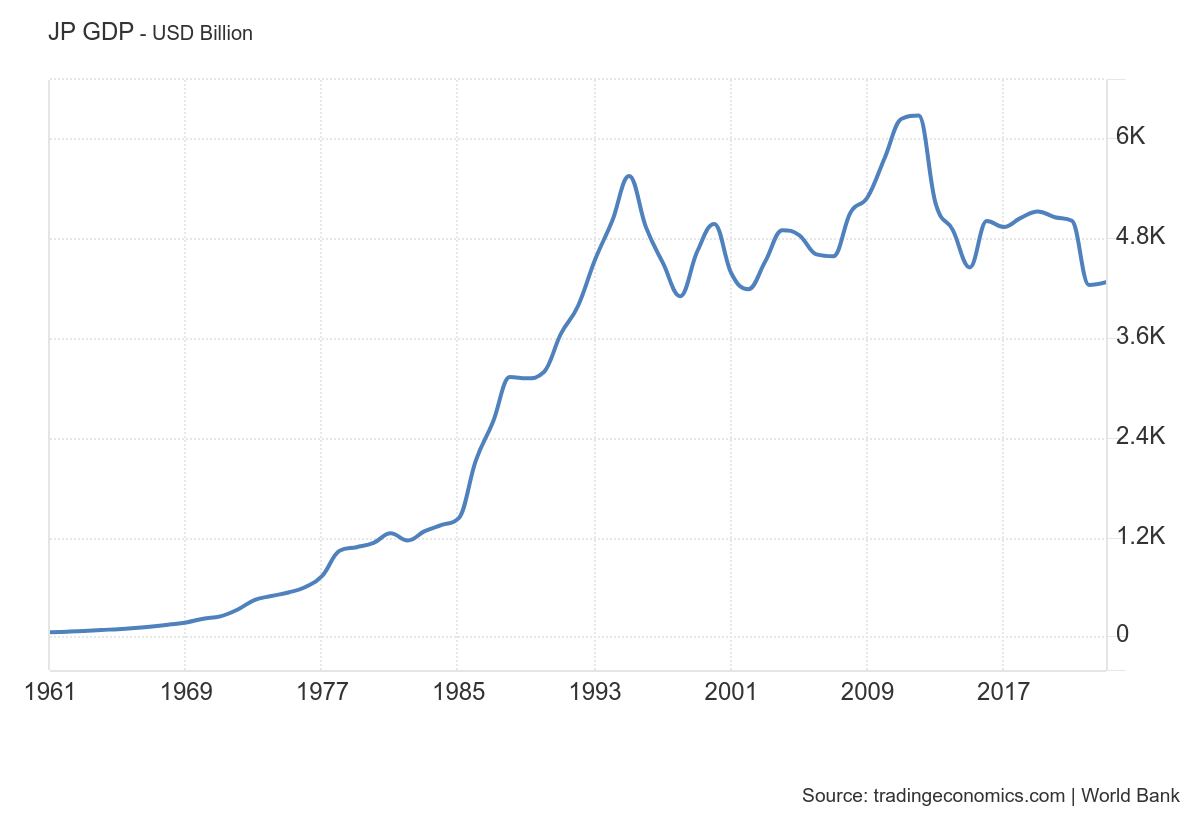

Japan, now the world's fourth largest economy in terms of nominal GDP, grew so rapidly in the previous century that it caused concern even in the United States. Since the 1990s, however, the country has been struggling with a number of problems. GDP measured in dollars is practically stuck at levels seen 30 years ago.

Source: TradingEconomics

Japan's economy, one of the largest in the world, has a number of problems that could hinder its growth. A major challenge is the ageing population - more than 36% of Japanese are 60 or older. This means there are fewer people to work with and rising healthcare and pension costs. Japan also has a huge debt, one of the highest in the world - 266% of its GDP.

Over the years in Japan, prices have been constantly falling, meaning we have had deflation. This discouraged people from spending and investing. Now the situation is starting to change, as inflation has risen to 2.8%. The Bank of Japan has tried to remedy this by buying a lot of assets since 2011 to raise inflation and reduce debt. This has had mixed results - inflation has not risen as fast as wanted, but it has helped reduce the debt problem somewhat.

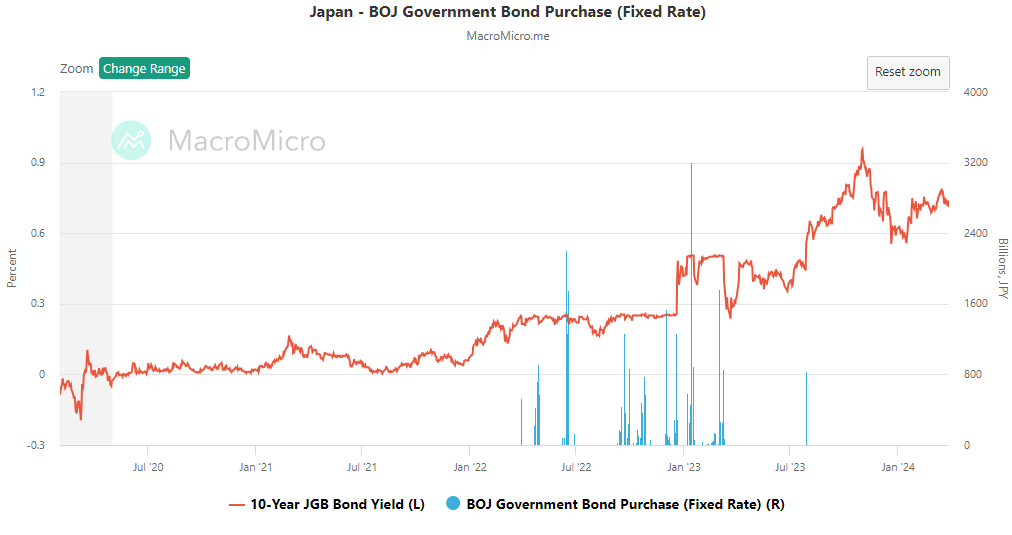

The Bank of Japan now holds as much as 54% of Japanese debt, a world record. However, the bank has decided to cut back on bond purchases, leading to a rise in bond yields from 0 to 0.7% - the biggest rise in a decade. As can be seen in the accompanying chart, recent bond market action (highlighted in blue) has failed to stem the current upward trend in Japan's bond yields (highlighted in red).

Source: MacroMicro

The Bank of Japan holds its hand over the intervention button!

In response to the weakening of the yen, which has pushed the currency to a 34-year low against the dollar, Japan's three main monetary authorities - the Bank of Japan, the Ministry of Finance and the Japan Financial Services Agency - met on Wednesday, 27 March, to discuss the yen's weakness and suggested a willingness to intervene in the market to prevent speculative currency movements. However, would this really be an effective measure?

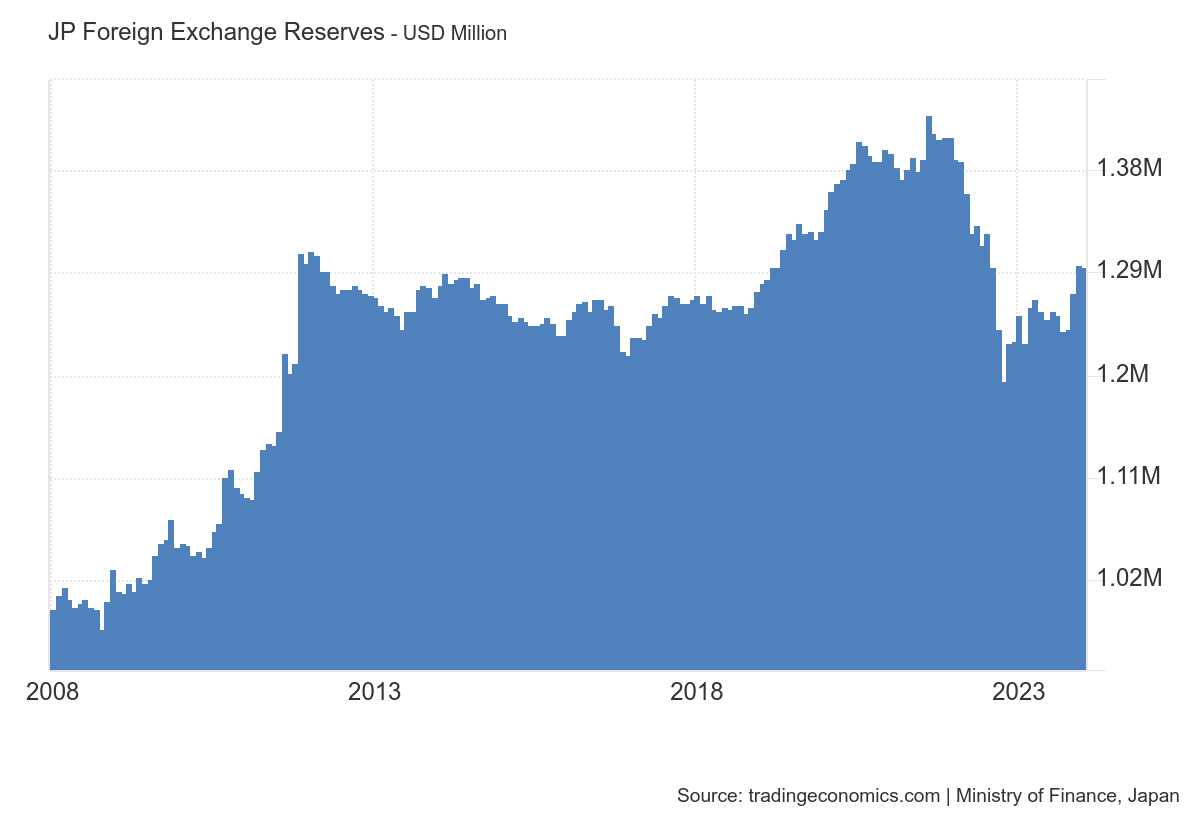

The last time the Bank of Japan intervened was in October 2022, when the yen reached lows near 152 per dollar. At that time, an estimated 9.2 trillion yen (about $60 billion) was spent to defend the exchange rate. Which effectively lowered the USD/JPY exchange rate by 16%, to around 128. This intervention accounted for approx. 4.6% of the foreign assets held by the Bank of Japan.

Source: Tradingeconomics

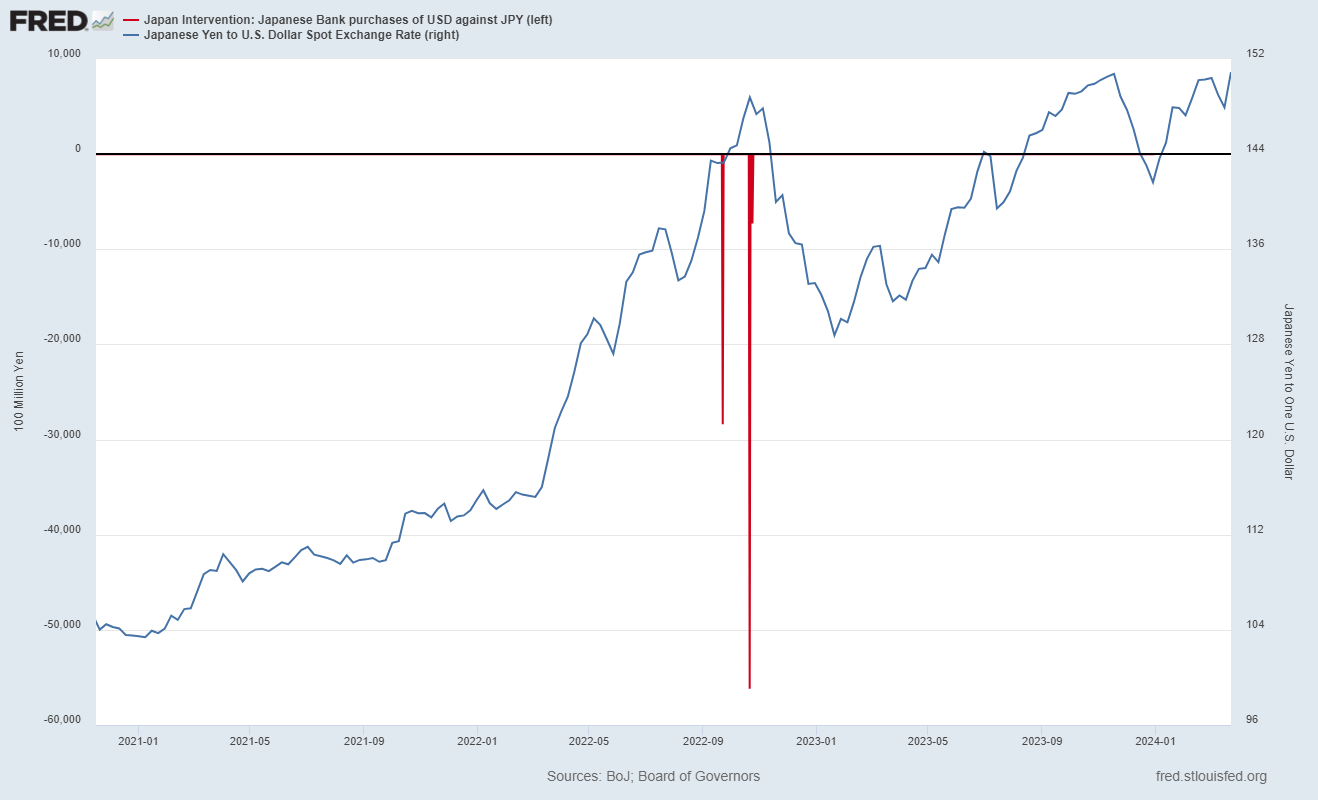

Since the cessation of the intervention, however, the weakening trend for the Japanese currency has not changed. It seems that a particularly important level for the USD/JPY pair here will be 152. Which has been defended by the market 3 times since the last intervention.

Source: Fred

The future of the Nikkei 225 and the USDJPY

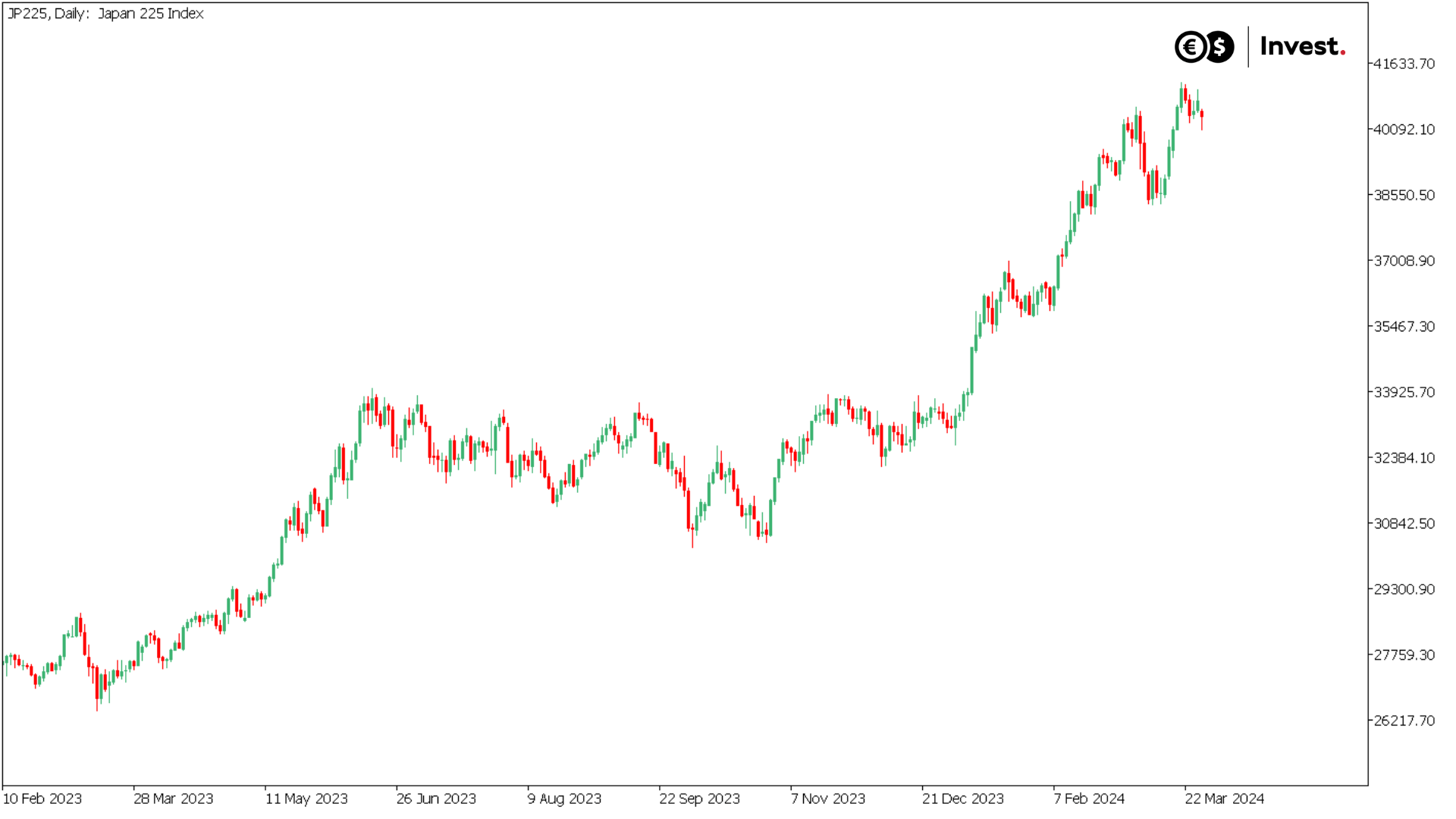

Typically, in economies where exports account for a significant share of GDP, a weakening of the domestic currency can have a positive impact on exporters' profits. The share of exports in Japan's GDP has been rising steadily, reaching 20% compared to 10.9% in the United States, for example. Consequently, the weak position of the yen is conducive to increasing profits for Japanese exporters, which include major corporations such as Toyota, Sony and Nintendo. Moreover, the emergence of price increases, or inflation, for the first time in decades is driving sales profits for many domestic companies. This resulted in an 8.5% increase in cumulative earnings per share in 2023 compared to the previous year.

Source: Conotoxia MT5, JP225, Daily

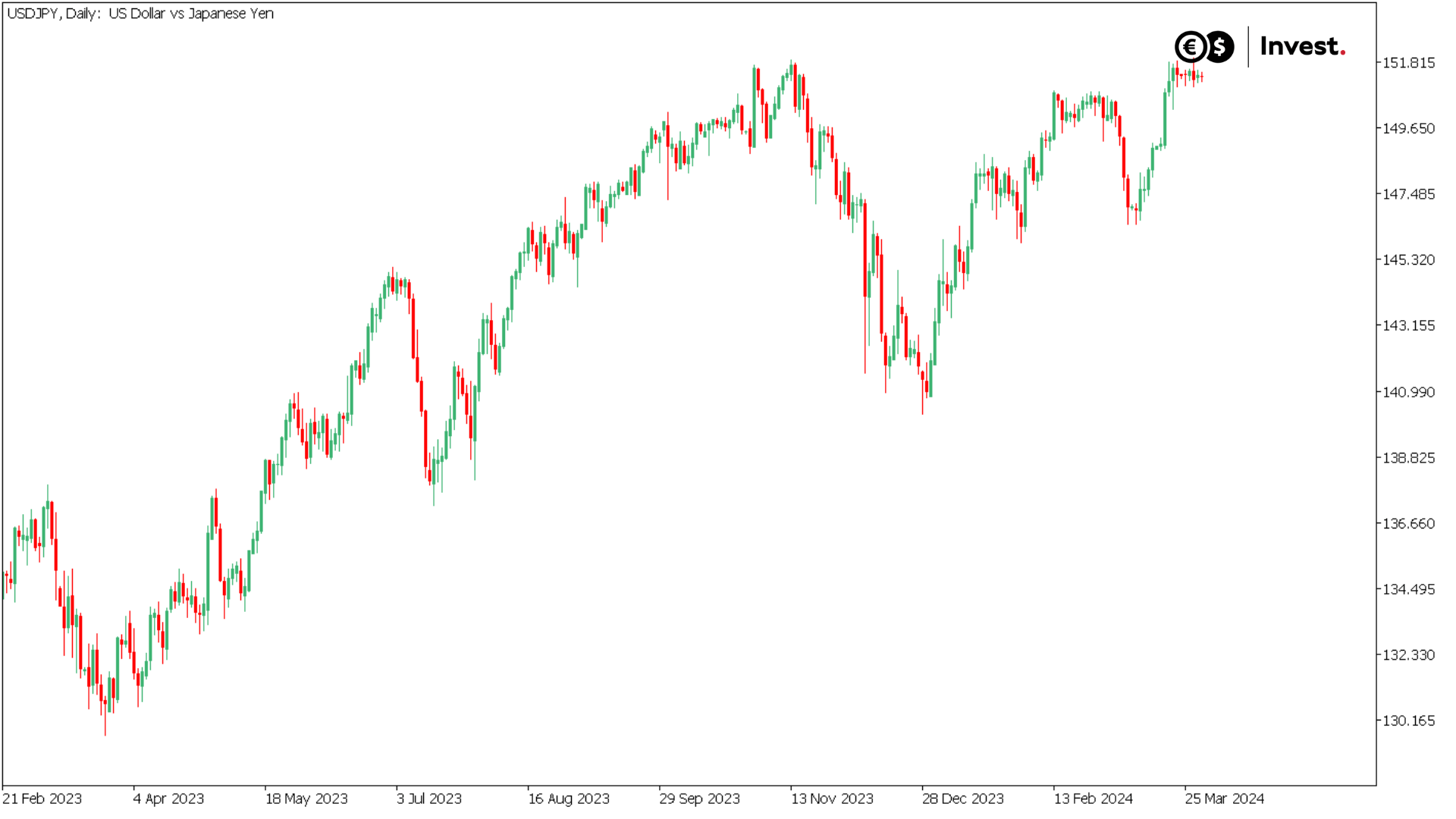

The situation in the USD/JPY currency market can be illustrated by the Bank of Japan holding its hand over the button 'marked intervention'. The Central Bank seems practically ready to act, which could bring the exchange rate back to the 140 level. However, it is worth emphasising that the Bank of Japan's ability to intervene is limited, especially in the context of raising interest rates. An increase in interest rates in Japan seems unlikely, as this could significantly increase the cost of new debt in a country that is already the most indebted developed country in the world. Consequently, verbal and monetary interventions remain the main tools.

The problem is that, in the scenario of abandoning intervention, Japan's continued reduction in bond purchases could maintain the tendency to weaken the yen, whose exchange rate in that case could be shaped mainly by the economy's declining competitiveness for decades.

Source: Conotoxia MT5, USDJPY, Daily

Grzegorz Dróżdż, CAI MPW, Market Analyst of Conotoxia Ltd. (Conotoxia investment service)

Materials, analysis and opinions contained, referenced or provided herein are intended solely for informational and educational purposes. Personal opinion of the author does not represent and should not be constructed as a statement or an investment advice made by Conotoxia Ltd. All indiscriminate reliance on illustrative or informational materials may lead to losses. Past performance is not a reliable indicator of future results.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71.98% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Trade this news from Conotoxia Ltd. platforms

Go to your account