Yields on 30-year US Treasury bonds briefly exceeded 5%. Such levels were last seen before the great financial crisis of 2008. Are we facing the harbinger of another major setback? Not necessarily. However, this does not mean that the situation is safe. After all, high interest costs mean that the long-term potential of western markets is beginning to melt away before our eyes, especially as developed countries are now in debt up to their eyeballs. Stimulating economies with further series of debt will be the most difficult since the beginning of this century. High long-term government bond yields have also pierced the multi-year corporate yield of the US S&P 500 index. If so, what could we expect in the financial markets and when will we see a reversal of this trend?

Table of contents:

- The future of interest rates

- Warren Buffet explains how interest rates affect the market

- Crisis in banks and real estate

The future of interest rates

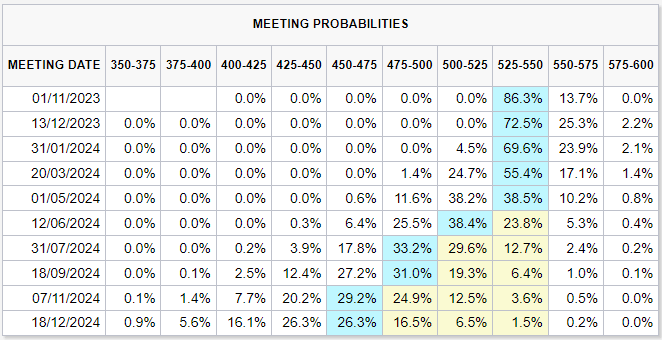

If we look at the probability of interest rate changes according to the CME FedWatch Tool, we can see that there are unlikely to be any more interest rate rises. The first reductions are forecast from March next year with a probability of 24.7%. This is of particular importance for the bond market, as their valuation depends very much on the expected level of interest rates. Even so, it is difficult to predict unequivocally how long interest rate increases on long-term debt will last. Nevertheless, should a recession occur, we are likely to see a drastic fall in yields, resulting from a reduction in interest rates.

Warren Buffet explains how interest rates affect the market

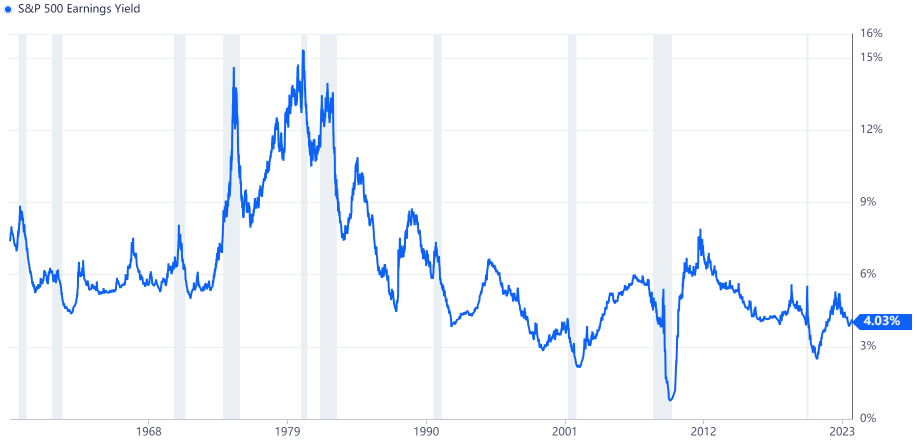

Warren Buffett aptly compared interest rates to gravity in the market. The higher the interest rates, the harder it is to achieve growth. This is because fewer projects become profitable. Therefore, companies that can sustain growth in such an environment can be considered solid. Currently, the yield on investments in companies from the S&P 500 index is 4.03%, which is 0.5% lower than the yield on 10-year US bonds. In the past, similar situations never lasted for long, as investments in equities always carry an additional risk, which must be reflected in the so-called risk premium. This term refers to the minimum expected return needed to cover this risk. Therefore, we can expect either a sudden increase in companies' earnings (which does not seem likely in view of the current crisis fears) or a drastic fall in bond yields.

Source: https://www.gurufocus.com/economic_indicators/151/sp-500-earnings-yield

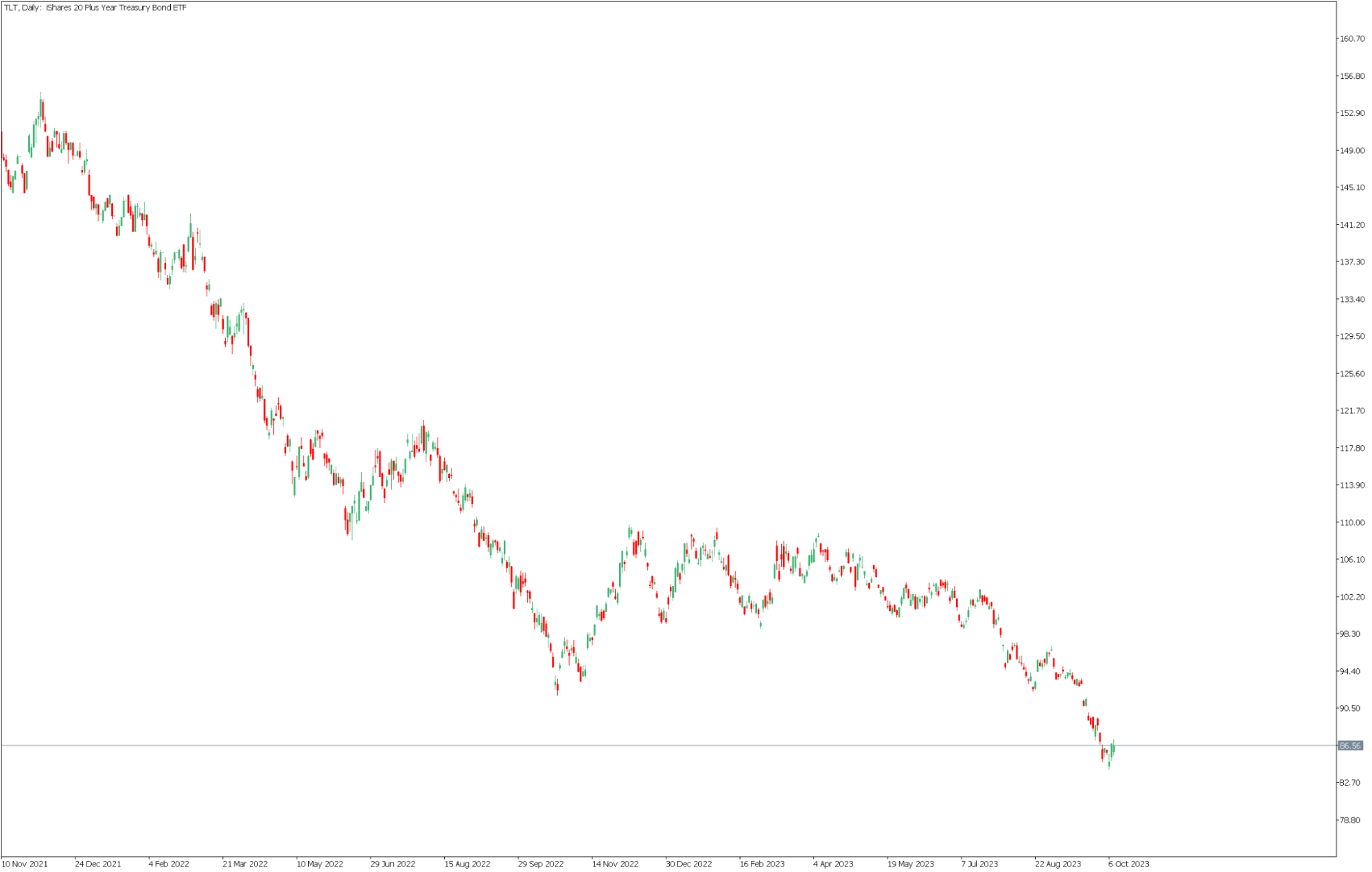

A fall in government bond yields would result in, among other things, a rise in the iShares 20 Plus Year Treasury Bond ETF (TLT), which is currently at its 16-year lows.

Source: Conotoxia MT5, TLT, Daily

Crisis in banks and real estate

The greatest impact of high bond yields is felt by the industry that has the most of these financial instruments in its portfolios. In particular, this is the financial sector, where banks often purchase long-term bonds in order to manage excess funds from customers and generate additional profits. As a result, the banking sector in the United States and Japan may be particularly vulnerable to selective fluctuations, especially for institutions that have not hedged against falling bond values.

The capital-intensive real estate industry is also not benefiting from rising funding costs. The US has already seen property prices fall by 10% and Germany by 6.7%, and it seems a matter of time before this spills over to the rest of the developed economies.

Grzegorz Dróżdż, CAI MPW, Market Analyst of Conotoxia Ltd. (Conotoxia investment service)

Materials, analysis and opinions contained, referenced or provided herein are intended solely for informational and educational purposes. Personal opinion of the author does not represent and should not be constructed as a statement or an investment advice made by Conotoxia Ltd. All indiscriminate reliance on illustrative or informational materials may lead to losses. Past performance is not a reliable indicator of future results.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.95% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Trade this news from Conotoxia Ltd. platforms

Go to your account